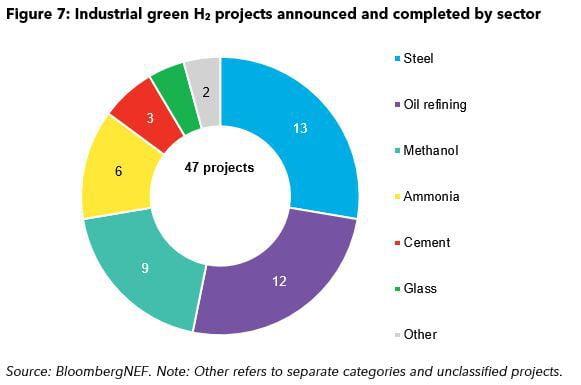

Clean hydrogen could help decarbonize many hard-to-abate sectors such as industry, heavy transport, power, and building heat. Many national hydrogen strategies emphasize industrial uses as a key demand sector. To date, European countries have been leading the charge and are likely to serve as a testing ground. The current pipeline of industrial projects focuses on sectors with limited potential for greater electrification or where clean H2 can replace existing demand for fossil fuel-derived H2, such as methanol, ammonia and refined oil products. The number of proposed industrial hydrogen clusters is also rising.

Transport

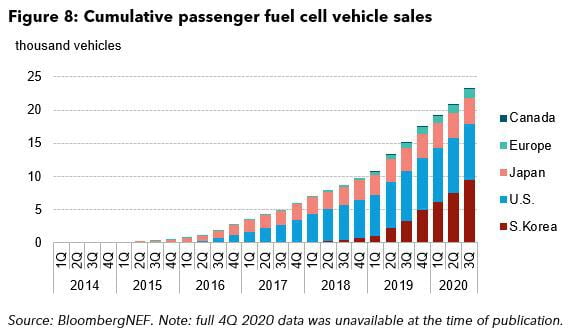

Fuel cell vehicles (FCV) have unfavorable economics compared to battery electric vehicles (EVs), so uptake of the technology is progressing slowly. At the end of 3Q 2020 there were just 23,290 passenger FCVs on the road, with the majority in South Korea, the U.S. and Japan. Sales of fuel cell buses and commercial vehicles have also been limited, but in the long term we expect fuel cell trucks to see higher sales as a share of the market compared to passenger FCVs, due to their better economics.

The rollout of refueling infrastructure has also been slow, with only 136 hydrogen refueling stations commissioned globally in 2020, just barely more than 2019. In the aviation sector, the number of hydrogen porotypes is growing, but H2 is unlikely to make a big dent in the aviation fuel

market as it takes five times as much space as conventional jet fuels.

Explore key findings from BNEF’s Electric Vehicle Outlook in a free public summary.

Power

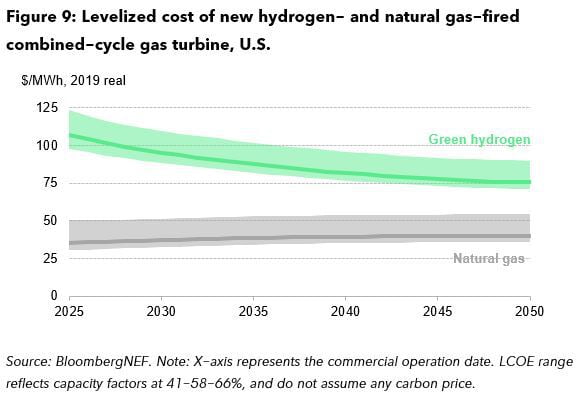

Hydrogen could be a key tool in managing the variability of solar and wind generation, complementing the short-duration capability of batteries. The cost of green H2 power generation is expected to remain above natural gas through 2050, although the difference will narrow.

Turbine manufacturers have already produced units of up to 50MW that can run on high blends of H2 at petrochemical sites. Recent announcements suggest some 8.9GW of hydrogen-ready gas turbines could be operating worldwide by 2028, with some projects set to be commissioned as early as 2021. Much of the activity is taking place in the U.S. due to state-level clean energy targets.

The Levelized Cost of Electricity analysis (available to clients on web & the Bloomberg Terminal) is our semi-annual assessment of the cost competitiveness of different power-generating and energy storage technologies across the world, including hydrogen.

Demand by 2050

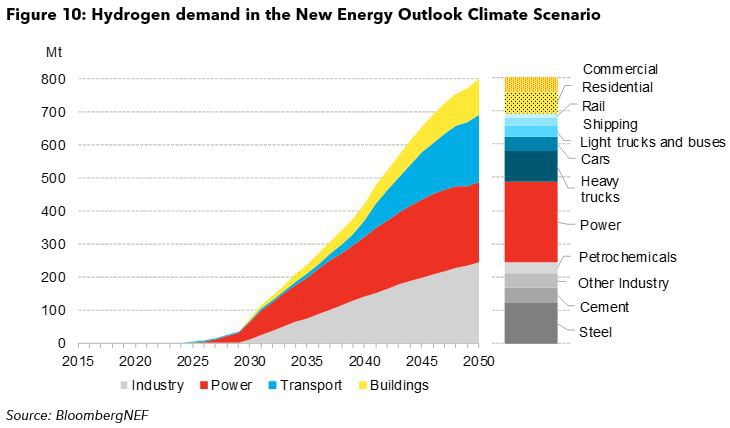

If long-term climate targets are to be met, hydrogen could play a major role in meeting the world’s energy needs. In our flagship New Energy Outlook, we examined a scenario where clean electricity and green hydrogen are used as the predominant technologies to limit warming to well below 2°C. Demand for hydrogen in this scenario amounted to 801 million tons in the year 2050, requiring 9.6TW of electrolyzers. Around 30% of this goes to power generation, another 30% goes to industry, 25% to transport and 15% to buildings.